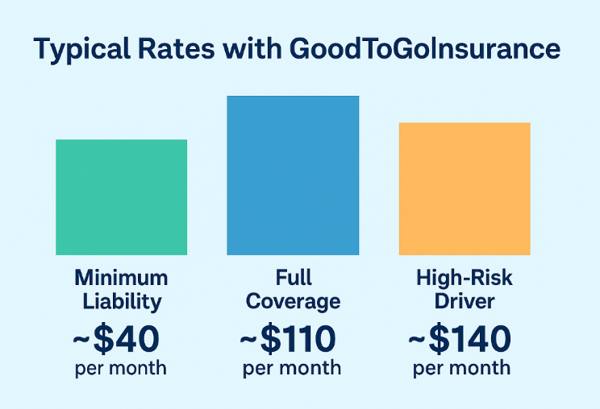

GoodToGoInsurance is best for drivers who need the cheapest coverage possible with the most discounts. Goodtogo auto insurance offers fast, flexible insurance without the complications that come with traditional providers.

Whether you’re dealing with a lapse in coverage, credit challenges, or simply want a more straightforward way to get insured, GoodToGoInsurance focuses on accessibility, speed, and affordability. Understanding the coverage options and discounts available through GoodToGoInsurance can help you decide whether it’s the right solution for your needs and how to keep your monthly cost as low as possible.

This guide breaks down GoodToGoInsurance coverage options in clear terms, explains how discounts work, and shows how drivers can maximize value while staying legally protected on the road.

Overview of GoodToGoInsurance Coverage

GoodToGoInsurance primarily focuses on essential auto insurance coverage that meets state minimum requirements while offering optional protections for drivers who want more security. The emphasis is on practical coverage rather than complicated bundles, making it easier for drivers to get insured quickly.

Unlike traditional insurers that require extensive underwriting and long approval processes, GoodToGoInsurance streamlines enrollment. Many drivers are approved the same day, making it a popular option for those who need immediate proof of insurance.

Liability Coverage Through GoodToGoInsurance

Liability insurance is the foundation of most auto insurance policies, and GoodToGoInsurance offers liability coverage that satisfies state-mandated minimums. This coverage helps pay for bodily injury and property damage if you are found at fault in an accident.

GoodToGoInsurance liability coverage is well-suited for drivers who:

- Need legal compliance to register or drive a vehicle

- Want affordable monthly payments

- Are not looking for high-cost, full-coverage plans

While liability-only coverage does not protect your own vehicle, it is often the most cost-effective way to stay insured, especially for older cars or drivers on a tight budget.

Collision Coverage Options

For drivers who want protection for their own vehicle, GoodToGoInsurance may offer collision coverage as an optional add-on, depending on availability in your state. Collision coverage helps pay for repairs or replacement if your vehicle is damaged in an accident, regardless of fault.

This type of coverage is particularly useful if:

- Your vehicle still has significant value

- You want peace of mind beyond minimum coverage

- You are financing or leasing your car

Adding collision coverage increases your premium, but it can prevent large out-of-pocket expenses after an accident.

Comprehensive Coverage Availability

Comprehensive coverage protects against non-collision events such as theft, vandalism, fire, falling objects, and weather-related damage. GoodToGoInsurance’s comprehensive options are typically chosen by drivers who live in high-risk areas or want broader protection.

This coverage can be especially valuable if you:

- Park your car on the street

- Live in an area prone to theft or extreme weather

- Want coverage beyond accidents

While not required by law, comprehensive coverage adds another layer of financial protection that many drivers find worthwhile.

Uninsured and Underinsured Motorist Coverage

GoodToGoInsurance may also provide uninsured or underinsured motorist coverage in states where it is required or commonly offered. This coverage helps protect you if you’re involved in an accident with a driver who has little or no insurance.

Given the high number of uninsured drivers nationwide, this option can be a smart addition for drivers who want extra protection without significantly increasing their premiums.

Medical Payments and Personal Injury Protection

Depending on your location, GoodToGoInsurance may offer medical payments coverage or personal injury protection. These options help cover medical expenses for you and your passengers after an accident, regardless of fault.

This type of coverage can help with:

- Emergency room visits

- Follow-up medical care

- Lost wages in some states

For drivers without strong health insurance, this coverage can provide critical financial support after an accident.

GoodToGoInsurance Discounts Explained

One of the biggest advantages of GoodToGoInsurance is its focus on affordability. Discounts play a major role in keeping premiums manageable, especially for drivers who may struggle to qualify for savings elsewhere.

While discounts vary by state and underwriting partner, common GoodToGoInsurance discounts may include:

These savings can add up quickly, especially when combined. Even small discounts can significantly reduce monthly costs over time.

Discounts for High-Risk and Non-Standard Drivers

GoodToGoInsurance is often appealing to non-standard drivers, including those with past violations, accidents, or lapses in coverage. While traditional insurers may deny coverage or charge extremely high rates, GoodToGoInsurance works with providers willing to insure higher-risk drivers.

Although high-risk drivers may not qualify for every discount, maintaining coverage and avoiding new violations can lead to better rates over time. Some drivers see noticeable improvements in pricing after six to twelve months of continuous coverage.

How to Maximize Savings With GoodToGoInsurance

Drivers can take several steps to lower their GoodToGoInsurance premium.

Comparing Coverage Value, Not Just Price

While GoodToGoInsurance is known for affordability, it’s still important to evaluate coverage value rather than focusing only on the lowest price. Understanding what is and isn’t covered can prevent surprises after an accident.

GoodToGoInsurance works best for drivers who want straightforward coverage without unnecessary extras. For many, the combination of essential protection, flexible payments, and accessible discounts makes it a practical choice.

Final Thoughts on GoodToGoInsurance Coverage and Discounts

GoodToGoInsurance coverage options are built around simplicity, speed, and affordability. From basic liability insurance to optional protections like collision and comprehensive coverage, drivers can customize a policy that fits their needs and budget.

Discount opportunities further enhance the value of GoodToGoInsurance, especially for drivers who maintain continuous coverage and responsible driving habits. While it may not offer every premium feature found with large national insurers, GoodToGoInsurance fills an important role for drivers who need reliable coverage without unnecessary barriers.

For drivers looking for a fast, accessible insurance solution, GoodToGoInsurance remains a strong option worth considering.