Very Cheap Car Insurance with No Deposit: Comprehensive Guide for 2025

Struggling to afford car insurance with a large upfront deposit? Very cheap car insurance with no deposit offers a solution for drivers needing immediate, affordable coverage without tying up funds. While most insurers require a 20–30% deposit, select providers in certain states offer zero-down or low-deposit plans starting at $20. This in-depth guide explores eligibility, providers, states, payment options, and strategies to secure the best rates. Enter your zip code to compare no-deposit insurance quotes and save.

Understanding No Deposit Car Insurance

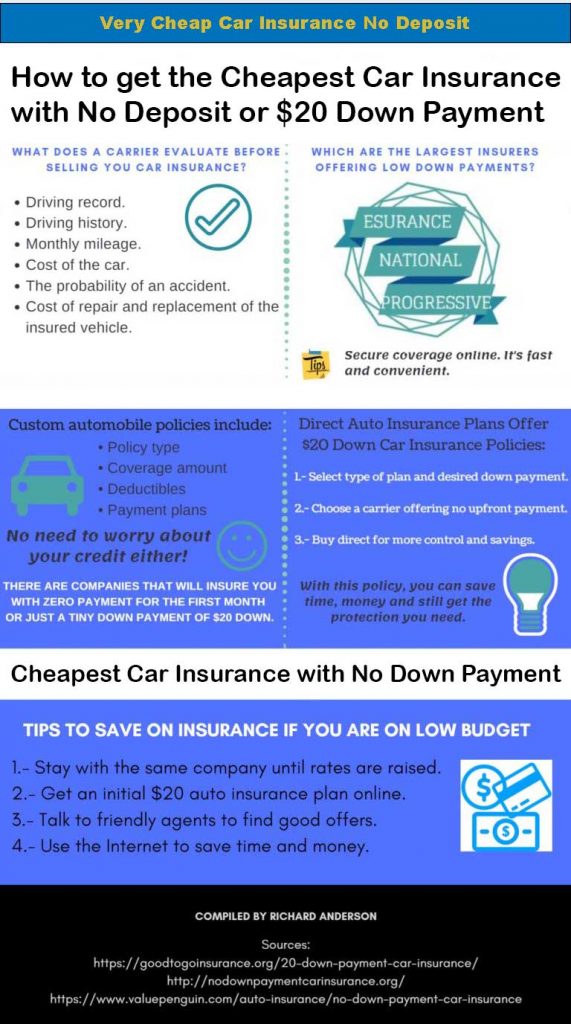

No deposit car insurance, often called zero-down insurance, allows drivers to activate a policy without an upfront deposit, using the first month’s premium as the initial payment. It’s not free insurance but reduces immediate costs, making it ideal for low-income households, students, or those purchasing new vehicles. Deposits typically depend on risk factors like driving history, vehicle type, and credit score. No-deposit plans are rare and limited to specific states, but low-deposit alternatives are widely available. Learn more about flexible insurance options.

Why No Deposit Insurance Is Popular

Financial constraints often force drivers to prioritize essential expenses, but auto insurance is legally required in most states. No-deposit policies address this by:

Eliminating large upfront payments

Offering monthly plans starting at $29

Allowing immediate, legal coverage

Freeing up cash for other necessities

These plans are especially appealing for low-income drivers or those recovering from financial setbacks. Compare rates with instant no-deposit quotes.

How No Deposit Insurance Works

Insurers typically offer two payment options: full premium upfront or monthly installments. With no-deposit plans, the first monthly payment doubles as the deposit, activating coverage without additional upfront costs. This structure minimizes financial strain but may result in higher monthly premiums due to increased insurer risk. For example, a $1,500 annual policy might cost $129/month with no deposit, compared to a one-time $1,470 payment. Start exploring with online quote tools.

Eligibility for No Deposit Plans

Not all drivers qualify for no-deposit insurance due to risk-based underwriting. To improve your chances, you should:

Be over 25 years old

Have a clean driving record (no DUIs, tickets, or at-fault accidents)

Maintain a credit score of 740 or higher

Drive a low-risk vehicle (e.g., sedans, not sports cars)

Have continuous coverage for three+ years

High-risk drivers, such as those with DUIs, may face deposits of 30% or more. Check eligibility for credit-friendly plans.

States Offering No Deposit Insurance

Due to state regulations, no-deposit auto insurance is only available in:

Arizona

California

Florida

Georgia

New York

Oklahoma

Washington

California, with nearly 40 million residents, has the most providers, offering competitive zero-down options. In other states, low-deposit plans starting at $20 are common alternatives. Compare rates in California or Georgia.

Top Providers for No Deposit Insurance

Several reputable insurers offer no or low-deposit plans, including:

Progressive: Zero-down options for drivers with 740+ credit; low deposits from $20.

Safe Auto: Budget-friendly no-deposit policies for basic coverage.

Kemper: Flexible payment plans in eligible states.

Allstate: Low-deposit plans with comprehensive options.

State Farm: Limited zero-down plans for low-risk drivers.

Nationwide: Competitive rates with flexible payments.

Travelers: Low-deposit options for safe drivers.

Farmers: Customizable plans with minimal deposits.

Note: USAA is exclusive to military members. Compare providers via top insurers.

Pros and Cons of No Deposit Insurance

Pros:

Immediate coverage without upfront costs

Flexible monthly payments starting at $29

Keeps cash available for other expenses

No cancellation penalties

Quick online quotes with 24/7 support

Cons:

Higher monthly premiums due to insurer risk

Limited availability by state and driver profile

Potential for policy cancellation if payments are missed

No-deposit plans increase monthly costs compared to paying in full, as shown below:

Cost Difference

No Deposit Plan

Paid in Full

1st Payment

$129

$1,470

Annual Cost

$1,548

$1,470

Amount Saved

$0

$78

Paying in full saves ~5%, and automatic monthly payments may offer small discounts. Learn about premium structures.

Customer Success Stories

No-deposit insurance has transformed affordability for many. A California single parent with a 2010 Honda saved $450/year with Safe Auto’s $30/month no-deposit plan. A Georgia family bundled two vehicles with Progressive, cutting costs by $600 annually using a zero-down policy. A Florida retiree switched to Kemper’s no-deposit plan for a 2008 SUV, saving $400/year. These examples highlight real-world savings. Compare Florida rates.

Strategies to Secure Cheap No Deposit Insurance

Maximize affordability with these tips:

Bundle Policies: Combine auto and home insurance for 10–15% savings.

Raise Deductibles: A $1,000 deductible can reduce premiums by 15%.

Apply Discounts: Qualify for safe driver, military, senior, or multi-car discounts.

Eliminate Overlaps: Skip rental car or roadside coverage if provided by credit cards or AAA.

Drive Safely: Avoid tickets and accidents to maintain low rates.

Choose Low-Risk Vehicles: Sedans or SUVs cost less to insure than sports cars.

Drivers aged 55–70 often qualify for no-deposit plans due to safe driving habits and lower mileage. Insurers like State Farm offer senior discounts, reducing rates and deposits. Explore senior insurance plans.

Young Drivers

Drivers under 25 face higher rates and deposits due to higher accident risks, often paying double what a 35-year-old does. Distracted driving (e.g., texting) increases costs. Low-deposit plans are more realistic than zero-down. Check youth insurance options.

High-Risk Drivers

Those with DUIs, multiple tickets, or poor credit may struggle to secure no-deposit plans, facing deposits up to 33%. Specialized providers offer low-deposit alternatives. See high-risk plans.

Choosing a Reliable Insurer

When selecting a no-deposit provider, consider:

Financial Stability: A.M. Best rating of A or higher ensures reliability.

Claim Efficiency: Fast, fair payouts are critical.

Reputation: Check Better Business Bureau for customer feedback.

Customer Support: 24/7 live assistance for claims and queries.

Digital Tools: User-friendly websites for quotes, payments, and claims.

Payment Flexibility: Options like automatic monthly payments.

Secure very cheap car insurance with no deposit today! Enter your zip code to compare quotes and drive legally.

heir lowest rates and minimum deposit requirements.

Many direct providers have some of the best rates available. Many consumers report saving $500 or more by buying a direct policy online. To compare the rates where you live, just enter your zip code and fill out a quick quote. It only takes about five minutes, and you can compare up to 10 quotes. Get started now and find the coverage you need at low rates you can afford.

Copyright1997 -

2026. All Rights Reserved. The goal of this site is to accurately match clients to the auto insurance companies that meet their intended needs. We don't sell any type of insurance and are not affiliated with one specific insurer.All trademarks remain the property of their actual holders.(Term: Very Cheap Car Insurance with No Deposit)